Byadmin

Byadmin

15 Financial Questions to Ask Before Marriage: A Complete Checklist

Share your love

Love Is Beautiful. Financial Surprises Are Not.

Here’s something nobody tells you at the engagement party: marriage is, among other things, a financial merger.

You’re not just combining your Netflix queues and bathroom cabinet space. You’re combining income streams, credit scores, spending habits, student loans, retirement accounts, and — if things go sideways — legal liability. That’s a lot riding on a conversation most couples never have before the wedding.

I get it. Talking about money feels awkward. It’s weirdly more intimate than talking about your childhood fears or your exes. But here’s the thing — couples who talk about money before marriage are significantly less likely to fight about it after. And fighting about money is one of the top predictors of divorce in the U.S.

So consider this your pre-marriage financial checklist. Fifteen questions. Real talk. No sugarcoating.

Let’s get into it.

Why Financial Conversations Before Marriage Actually Matter

According to a survey by Ramsey Solutions, money fights are the second leading cause of divorce in America, right behind infidelity. And yet, a 2023 Fidelity Investments Couples & Money Study found that 43% of couples don’t know their partner’s salary — even after years together.

That’s wild, right?

The point isn’t to interrogate your partner like you’re an IRS auditor. It’s to understand who you’re building a life with — financially speaking. Because your partner’s money habits will directly affect your credit score, your savings goals, your stress levels, and your future kids’ college fund. No pressure.

The 15 Financial Questions to Ask Before Marriage

1. What Is Your Current Income — and How Stable Is It?

This one seems obvious, but you’d be surprised how many couples dance around it. Knowing your partner’s income isn’t about judgment — it’s about planning reality.

Ask:

- Is your income salaried, hourly, freelance, or commission-based?

- How stable has it been over the past few years?

- Are there seasonal fluctuations?

A couple where one person earns $95K with full benefits and another earns $40K with irregular freelance gigs needs a very different budget strategy than two stable salaried earners. Know what you’re working with before you co-sign a mortgage.

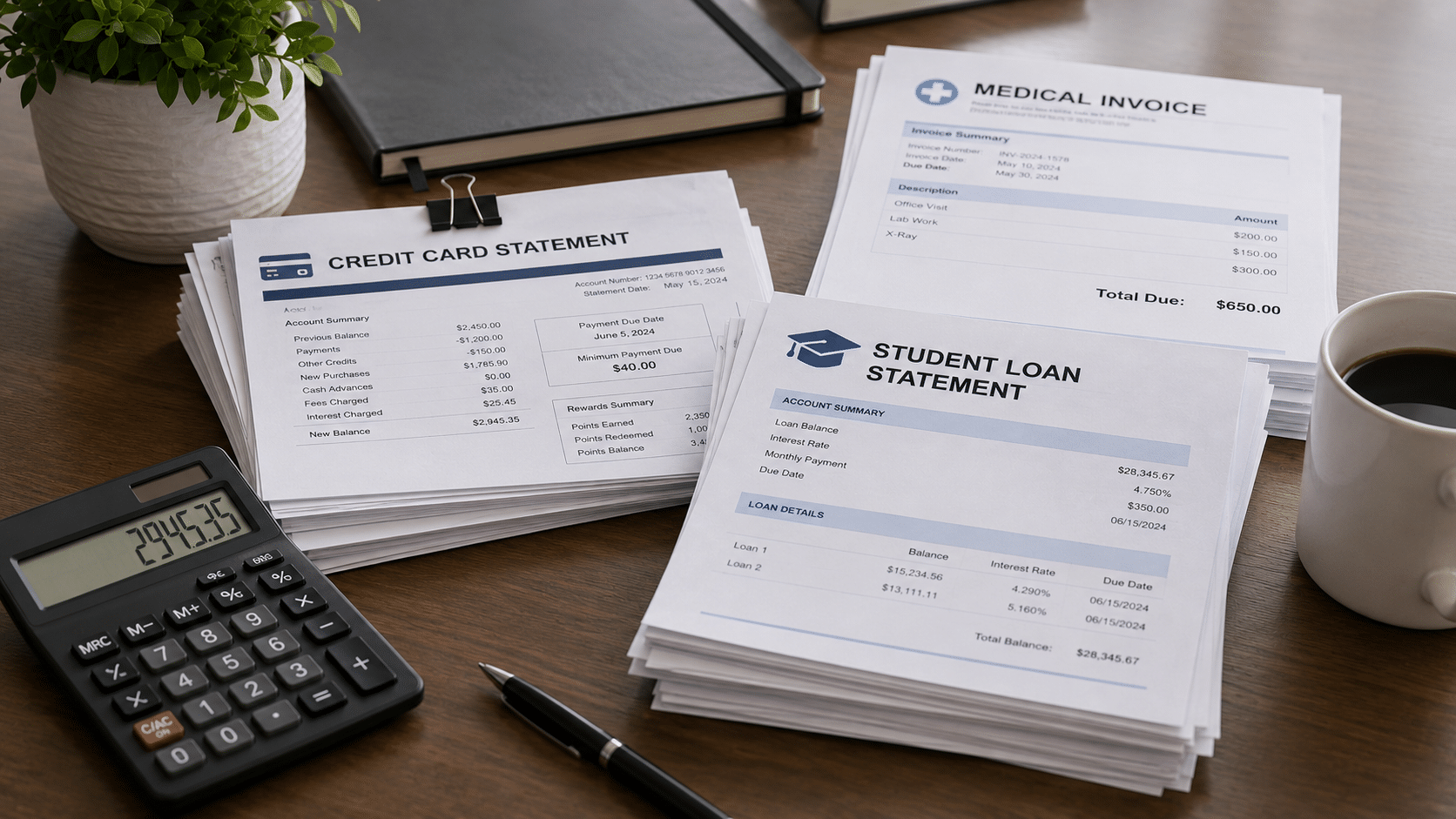

2. How Much Debt Are You Carrying?

Student loans. Credit card balances. Car payments. Medical bills. Personal loans from college. Debt is everywhere — and it doesn’t disappear when you get married.

Here’s what you need to ask:

- What types of debt do you have?

- What are the balances and interest rates?

- What’s your current monthly payment?

Tip: In most states, debt brought into a marriage stays with the individual who incurred it. But jointly taken debt — like a mortgage or a car loan after the wedding — is shared. Know the difference.

| Debt Type | Usually Individual | Can Become Joint |

|---|---|---|

| Student Loans (pre-marriage) | ✅ Yes | Only if refinanced jointly |

| Credit Card Debt (pre-marriage) | ✅ Yes | Only if added as joint holder |

| Mortgage (post-marriage) | ❌ No | ✅ Yes |

| Car Loan (post-marriage) | ❌ No | ✅ Yes |

3. What Does Your Credit Score Look Like?

Your partner’s credit score will affect your ability to buy a home together, get favorable loan rates, and even rent an apartment. It’s not shallow — it’s practical.

A good credit score (typically 700+) unlocks lower interest rates. A poor one can cost you tens of thousands of dollars over the life of a mortgage. Have this conversation early, without shame. If one partner has struggled with credit, that’s fixable — but only if you know about it.

4. Are You a Spender or a Saver — and Why?

This is the one that gets philosophical. Money behavior isn’t just about math. It’s about how you were raised, what money meant in your home, and what security looks like to you.

A person who grew up poor might hoard savings obsessively. A person who grew up wealthy might spend freely because they never had to think about it. Neither is inherently wrong — but if you’re opposites, you need a system.

Ask each other:

- Do you tend to spend or save by default?

- What does financial security feel like to you?

- Did money cause stress in your childhood home?

Understanding the why behind spending habits is way more useful than just knowing the what.

5. What Are Your Short-Term and Long-Term Financial Goals?

Before you merge your lives, you need to know if you’re heading in the same direction. Do you both want to own a home? Travel frequently? Retire early? Start a business?

Misaligned goals = constant financial conflict.

Make a list together:

- Short-term (1–3 years): Emergency fund, wedding costs, new car, vacation

- Mid-term (3–10 years): Down payment on a home, having children, starting a business

- Long-term (10+ years): Retirement, college savings, generational wealth

There’s no wrong answer — just mismatched ones.

6. Will We Combine Finances, Keep Them Separate, or Do Both?

There’s no universal right answer here. Some couples do everything jointly. Others keep completely separate accounts. Many use a hybrid system — shared account for bills and savings, individual accounts for personal spending.

The three main models:

| Model | How It Works | Best For |

|---|---|---|

| Fully Combined | All income goes into shared accounts | Couples with similar incomes & spending styles |

| Fully Separate | Each person handles their own finances | High earners, second marriages, independent types |

| Hybrid | Shared account for shared expenses + personal accounts | Most couples — offers flexibility and autonomy |

Decide this before the wedding. Seriously.

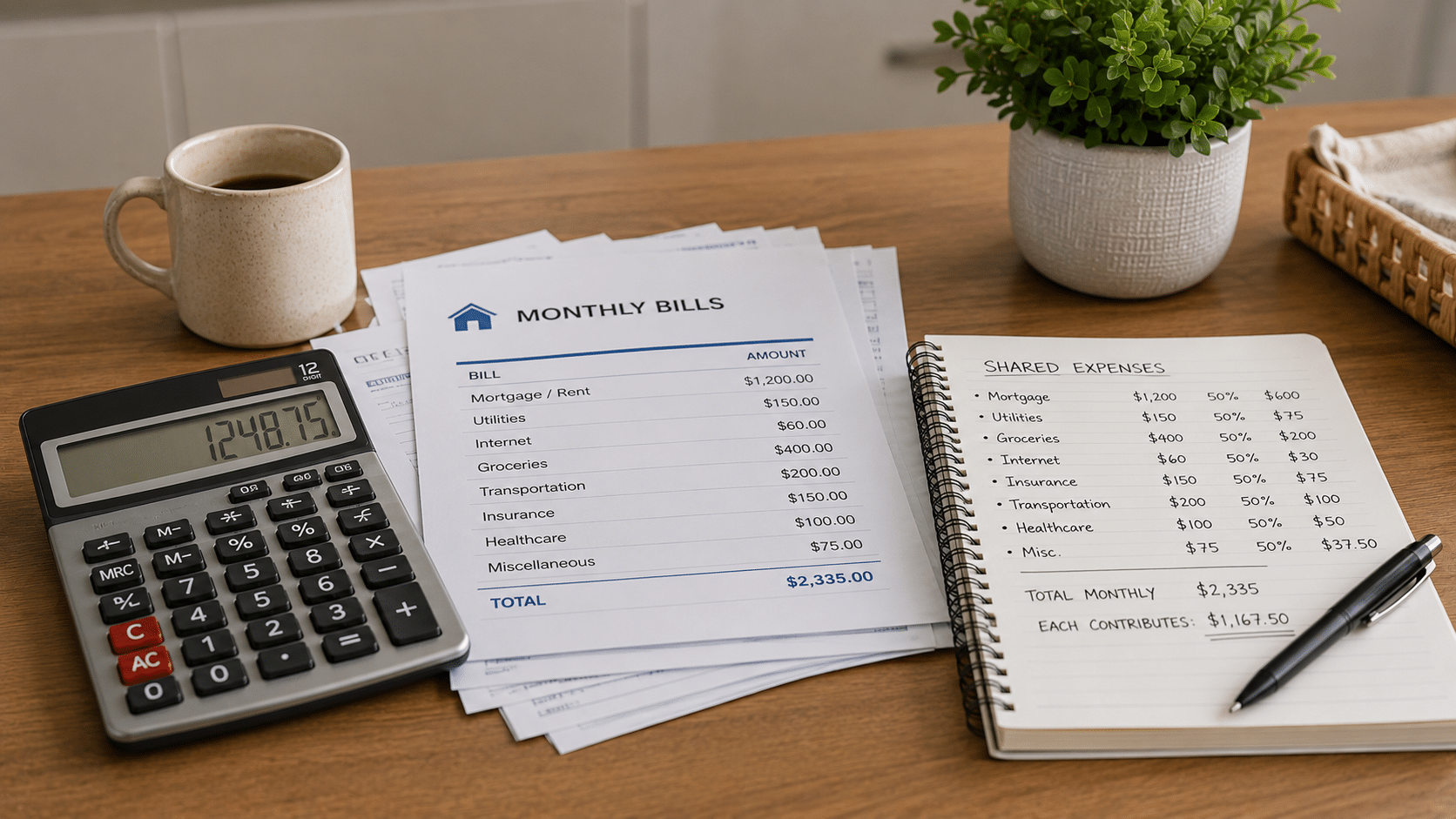

7. How Will We Handle Household Expenses — Split 50/50 or Proportionally?

This question gets spicy when incomes are unequal. If one partner earns $120K and the other earns $45K, splitting everything 50/50 can feel deeply unfair.

Proportional splitting — where each person contributes based on their percentage of combined income — tends to feel more equitable.

Example:

- Partner A earns $120K (73% of combined income)

- Partner B earns $45K (27% of combined income)

- Monthly shared expenses = $4,000

- Partner A contributes $2,920 / Partner B contributes $1,080

It’s math, not a power move. Talk about it openly.

8. Do You Have a Budget? Do You Actually Stick to It?

Having a budget is great. Actually using one is rarer than people admit.

Ask your partner:

- Do you track your spending?

- What budgeting method, if any, do you use?

- What happens when you overspend in a category?

Common budgeting methods:

- 50/30/20 Rule — 50% needs, 30% wants, 20% savings

- Zero-Based Budgeting — Every dollar is assigned a job

- Envelope System — Cash divided into categories

- Pay Yourself First — Savings auto-transferred before spending

If one of you is a meticulous spreadsheet person and the other hasn’t balanced a checkbook in five years, you’ll need to meet in the middle.

9. What’s Your Relationship With Saving for Emergencies?

Financial advisors recommend having 3–6 months of living expenses in an emergency fund. Most Americans don’t have that. In fact, a 2024 Bankrate survey found that only 44% of Americans could cover a $1,000 emergency from savings.

Ask your partner:

- Do you have an emergency fund?

- How many months of expenses does it cover?

- Where is it kept (savings account, money market, etc.)?

If neither of you has one, that’s your first joint financial goal. Full stop.

10. Are You Saving for Retirement — and How Much?

The earlier you start, the more you benefit from compound interest. This isn’t a lecture — it’s a mathematical fact.

Questions to ask:

- Do you have a 401(k) or IRA?

- Are you contributing enough to get your employer match (if applicable)?

- What’s your current retirement balance?

- At what age do you want to retire?

Quick retirement reality check:

| Age | Recommended Retirement Savings (Fidelity Guideline) |

|---|---|

| 30 | 1x your annual salary |

| 40 | 3x your annual salary |

| 50 | 6x your annual salary |

| 60 | 8x your annual salary |

| 67 | 10x your annual salary |

If either of you is behind, that’s okay — but you need to know so you can plan together.

11. Do You Have Life Insurance or Any Other Insurance?

This one doesn’t feel romantic, but it’s genuinely an act of love.

Ask:

- Do you have life insurance? How much coverage?

- Do you have health, disability, or renter’s/homeowner’s insurance?

- Will we stay on separate plans or combine where possible?

Once you’re married, you can often add a spouse to health insurance during open enrollment. This could save thousands annually — but you need to compare plans to find the better deal.

12. Have You Ever Filed for Bankruptcy or Faced Serious Financial Hardship?

This can feel like a deeply personal question, and it is. But it matters.

A bankruptcy on a credit report can affect your joint financial decisions for years. It doesn’t disqualify someone from being a great partner — life happens — but it does need to be disclosed before marriage, not discovered after.

Have this conversation with compassion, not judgment. Ask:

- Have you ever had accounts sent to collections?

- Have you ever filed for bankruptcy?

- Are there any liens, garnishments, or legal financial judgments against you?

Trust is built on transparency.

13. Do You Believe in Prenuptial Agreements?

Let’s take the stigma out of this one. A prenup isn’t a sign of distrust — it’s a legal document that clarifies financial expectations and protects both parties.

Prenups are especially worth considering if:

- One or both partners have significant assets or debts

- Either partner has children from a previous relationship

- One partner owns a business

- There’s a major income disparity

The conversation itself is valuable, even if you ultimately decide not to get one. It forces you to discuss ownership, inheritance, and financial roles explicitly.

14. What Happens to Finances If We Have Children?

Whether you plan to have kids or not, it’s a conversation worth having — because children are enormously expensive and wildly change your financial picture.

Ask:

- Will both of us continue working after having kids?

- How will we handle childcare costs?

- Are we planning to start a college savings fund (like a 529 plan)?

- How will parental leave affect our income?

According to the USDA, raising a child to age 18 costs an average of $310,000 in the U.S. That’s before college. Plan accordingly.

15. What Are Your Financial Dealbreakers?

Everybody has them — they just don’t always say them out loud.

Some people can’t be with someone who has gambling tendencies. Others won’t tolerate financial secrecy. Some need a partner who’s aggressively saving for early retirement. Others want the freedom to spend without answering for every latte.

Ask each other openly:

- What financial behaviors would seriously concern you in a partner?

- Are there things you’ve seen in past relationships that you’d never want again?

- What does financial respect look like to you?

This is the most honest conversation on the list. And probably the most important.

A Handy Pre-Marriage Financial Checklist

Here’s a quick summary you can actually use:

- Shared income figures and sources

- All existing debts (type, balance, interest rate)

- Credit scores for both partners

- Spending and saving personality

- Short, mid, and long-term financial goals

- How finances will be structured (combined, separate, hybrid)

- How shared expenses will be split

- Budgeting approach and habits

- Emergency fund status

- Retirement savings and goals

- Insurance coverage

- Any past financial hardships or bankruptcies

- Stance on prenuptial agreements

- Financial plan for children (if applicable)

- Financial dealbreakers

FAQs: Financial Questions Before Marriage

When should couples have financial conversations before marriage?

Ideally, well before the engagement — or at minimum, several months before the wedding. You want time to work through differences, make adjustments, and set up systems without the pressure of a looming date.

Is it rude to ask your partner about their debt before marriage?

Not at all. It’s responsible. Approach the conversation from a place of partnership, not judgment. Frame it as: “I want us to go into this together with full information.”

Do I inherit my spouse’s debt when we get married?

Generally, no — pre-marital debt stays with the individual. However, joint debt taken on after marriage is shared. Always consult a financial advisor or attorney for state-specific guidance.

What if we disagree on financial goals?

That’s normal. The key is identifying where you agree, where you compromise, and where you establish independent financial space. A fee-only financial planner can help couples navigate major disagreements.

Should we see a financial advisor before getting married?

It’s a great idea, especially if either partner has significant assets, debts, or children from a prior relationship. A session or two with a fee-only certified financial planner (CFP) can be incredibly clarifying.

Final Thoughts: Have the Conversation

Here’s the truth: no conversation kills a relationship faster than financial secrets discovered after the wedding. But an honest money talk before you say “I do”? That can actually bring you closer.

It shows you’re serious. It shows you respect your partner enough to be real with them. And it sets the foundation for a relationship built on transparency, not financial landmines waiting to go off at the worst possible time.

So pour yourself a glass of wine — or coffee, no judgment — sit down with your person, and work through this list. It might feel awkward for about five minutes. And then it’ll feel like the most mature, loving thing you’ve done as a couple.

Your future selves will thank you.

Did this checklist help? Share it with an engaged couple who needs to hear it. And if you’ve already had these conversations — we want to know how it went. Drop your experience in the comments below.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Consult a certified financial planner or attorney for guidance specific to your situation.